2026

Covariate-adjusted statistical dependence representation through partial copulas: bounds and new insights

Vinícius Litvinoff Justus, Felipe Fontana Vieira

ArXiv preprint 2026 Spotlight

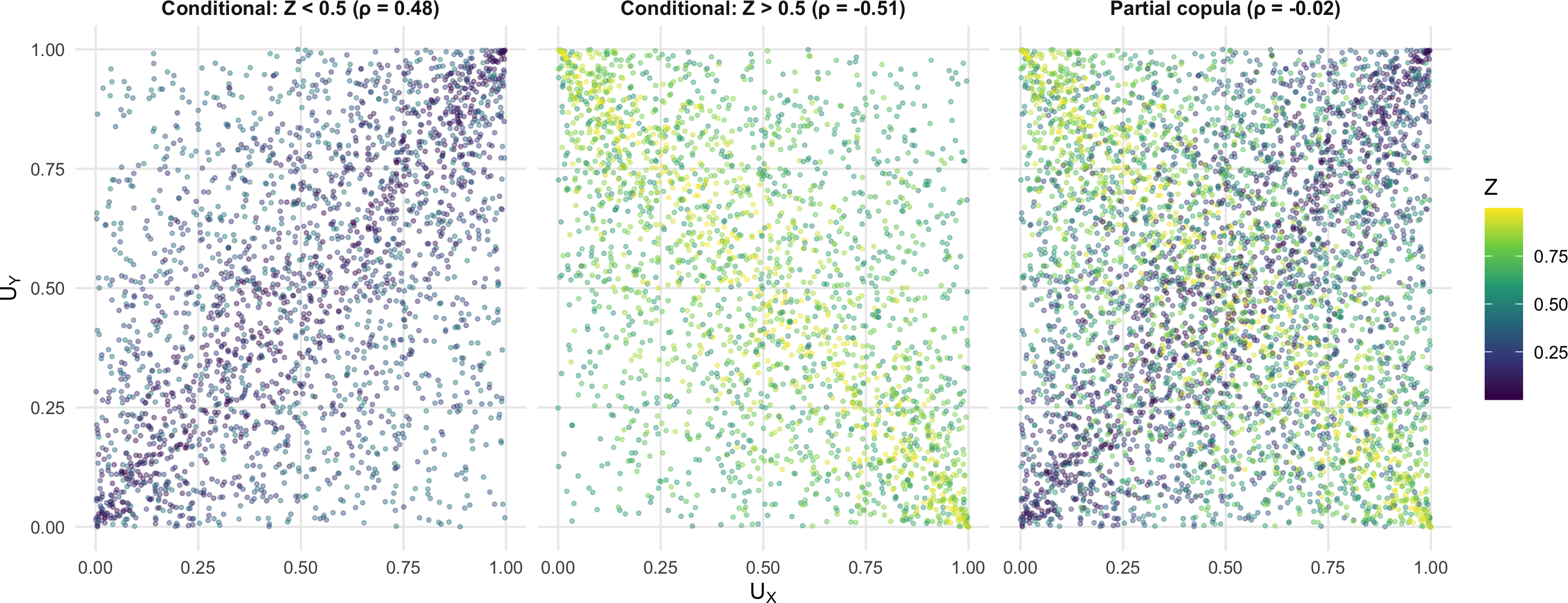

In this paper, we revisit the notion of partial copula, originally introduced to test conditional independence, highlighting its capability to represent the dependence between two random variables after removing their dependence with a covariate. Building upon results previously presented in the literature, we show that partial copulas can be seen as a nonlinear analogue of partial correlation. Then, we prove several results showing how dependence properties of the conditional copulas constrain the form of the partial copula. Finally, a simulation study is conducted to illustrate the results and to show the potential of partial copula as a way to describe covariate-adjusted statistical dependence. This highlights the potential of the method to be used in causal inference problems and recover the true sign of a causal effect.

Covariate-adjusted statistical dependence representation through partial copulas: bounds and new insights

Vinícius Litvinoff Justus, Felipe Fontana Vieira

ArXiv preprint 2026 Spotlight

In this paper, we revisit the notion of partial copula, originally introduced to test conditional independence, highlighting its capability to represent the dependence between two random variables after removing their dependence with a covariate. Building upon results previously presented in the literature, we show that partial copulas can be seen as a nonlinear analogue of partial correlation. Then, we prove several results showing how dependence properties of the conditional copulas constrain the form of the partial copula. Finally, a simulation study is conducted to illustrate the results and to show the potential of partial copula as a way to describe covariate-adjusted statistical dependence. This highlights the potential of the method to be used in causal inference problems and recover the true sign of a causal effect.

2024

Modeling structural causal equations via copulas

Vinícius Litvinoff Justus

Master's thesis (University of Campinas) 2024

This work is an effort towards the goal of understanding the connection between the concepts of causality and statistical dependence. Formally, this was done employing the notions of copula function and structural causal model. To achieve such goals, this dissertation first presented some problems that may arise in the analysis of non-experimental data and then presented the concepts of copula function and structural causal model. Within this context, this dissertation presented two contributions: first, based on the concept of structural equation, a copula-based procedure to control omission variable bias in linear models was presented (which is an extension of a method already present in the literature in the case of a Gaussian copula). Finally, the main contribution of this dissertation was done through representation theorems that enables seeing the impact of a causal intervention in a joint density probability function through a copula function. It was proved that the change in the joint density induced by the causal intervention is fully characterized by a copula function.

Modeling structural causal equations via copulas

Vinícius Litvinoff Justus

Master's thesis (University of Campinas) 2024

This work is an effort towards the goal of understanding the connection between the concepts of causality and statistical dependence. Formally, this was done employing the notions of copula function and structural causal model. To achieve such goals, this dissertation first presented some problems that may arise in the analysis of non-experimental data and then presented the concepts of copula function and structural causal model. Within this context, this dissertation presented two contributions: first, based on the concept of structural equation, a copula-based procedure to control omission variable bias in linear models was presented (which is an extension of a method already present in the literature in the case of a Gaussian copula). Finally, the main contribution of this dissertation was done through representation theorems that enables seeing the impact of a causal intervention in a joint density probability function through a copula function. It was proved that the change in the joint density induced by the causal intervention is fully characterized by a copula function.